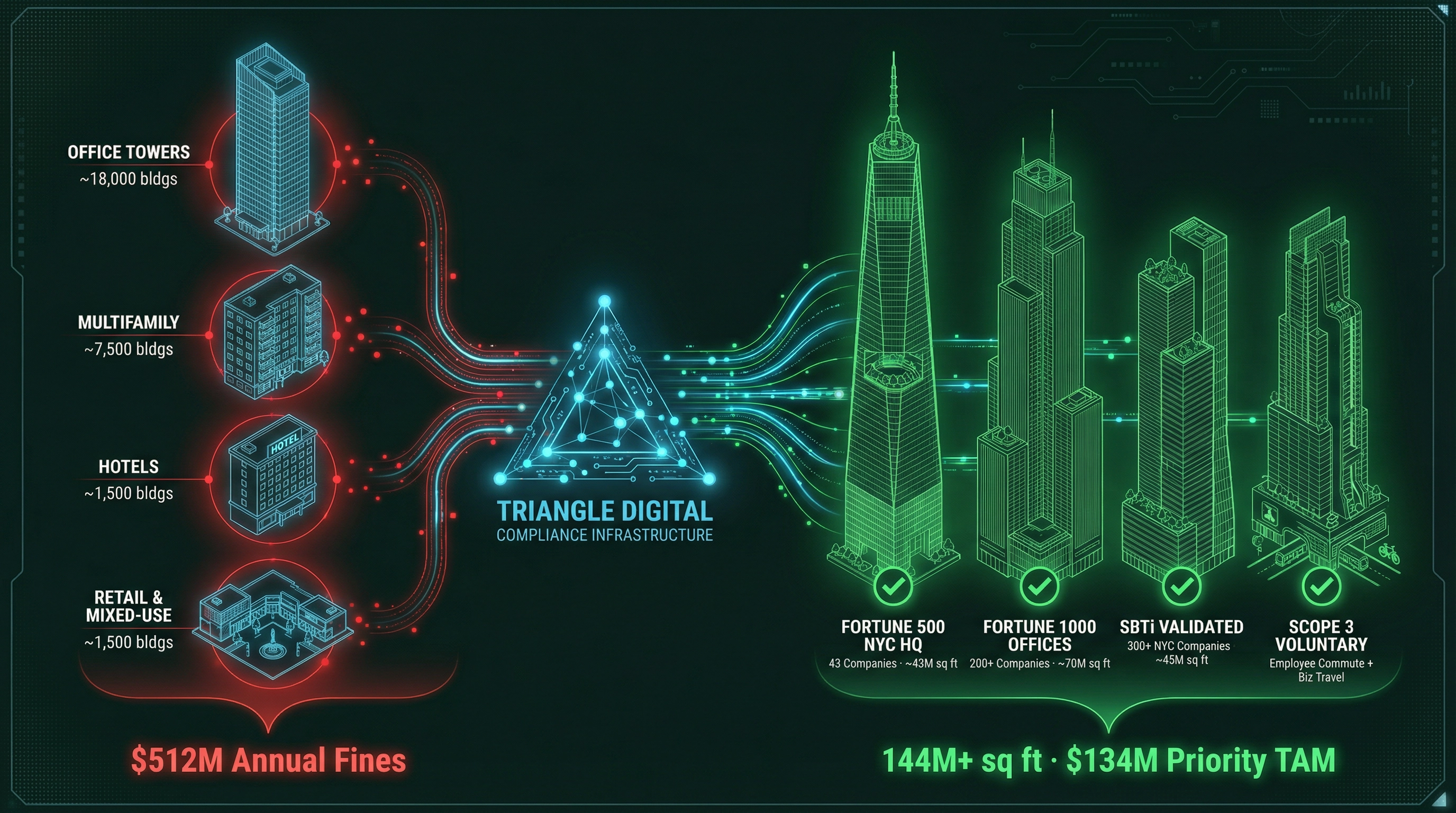

The Scale of the Compliance Challenge

LL97 applies to approximately 50,000 buildings across New York City. The law's phased emissions caps create dramatically different compliance dynamics depending on how the tightening schedule is structured.

Carbon Reduction Requirements by Phase

LL97 mandates a −40% reduction by 2030 and net-zero by 2050 relative to 2005 baselines. Limits are set as absolute emissions intensities (tCO₂e/sq ft) — not percentage cuts from a building's own baseline — meaning older, less efficient buildings face the steepest reductions.

Emissions Intensity Limits by Building Type (tCO₂e / sq ft)

Source: NYC Admin Code §28-320; 1 RCNY §103-14; Henderson Engineers (Jan 2024). Phase 3–5 limits projected.

| Building Type | 2024–2029 | 2030–2034 | Phase 2 Cut | Cumul. vs 2005 | 2035–2039* | 2040–2049* |

|---|---|---|---|---|---|---|

| Office (B) | 0.00846 | 0.00453 | −46% | ~58% | ~0.0030 | ~0.0015 |

| Multifamily (R-2) | 0.00675 | 0.00407 | −40% | ~49% | ~0.0027 | ~0.0013 |

| Hotel (R-1) | 0.01220 | 0.00598 | −51% | ~60% | ~0.0040 | ~0.0020 |

| Retail (M/A-2) | 0.01050 | 0.00420 | −60% | ~65% | ~0.0028 | ~0.0014 |

| Healthcare (I-2) | 0.02140 | 0.01050 | −51% | ~56% | ~0.0070 | ~0.0035 |

| Warehouse (S) | 0.00420 | 0.00210 | −50% | ~58% | ~0.0014 | ~0.0007 |

The law does not require a uniform percentage reduction from each building's own emissions. It sets an absolute cap that tightens over time. A 1960s-era office tower burning #4 fuel oil may need to cut its actual emissions by 60–70% just to meet the 2030 limit — while a modern LEED-certified tower may already comply through 2034 with no changes. The 2030 phase transition requires a 40–60% reduction in allowable intensity in a single year, sweeping 24,500 additional buildings into non-compliance overnight.

LL97 Six Phases to Achieve Net-Zero

LL97 establishes phased compliance thresholds tightening every five years from 2024 through 2050.

- Cliff Avg %

- Smoothed Avg %

- Carbon Footprint (MtCO₂e)

NYC Citywide GHG Reduction: 2024–2050

NYC building sector emissions (MtCO₂e) declining from the 2024 baseline of 58 MtCO₂e as each LL97 phase tightens limits. The blue dashed line shows the accelerated impact when Fortune 1000 and SBTi companies proactively cover their carbon footprint.

- LL97 Smoothed

- Smoothed + F1k/SBTi

- LL97 As-Written (Cliff)

Building Penalty Calculator

Estimate your building's LL97 fine exposure for 2024 (Phase 1) and 2030 (Phase 2 — Cliff), and see how a smoothed annual tightening program would reduce that burden. Compare the cost of paying the fine against purchasing Triangle Digital compliance credits.

Improving LL97

Addressing structural flaws for market adoption — four critical reforms needed to ensure the long-term viability and success of NYC's decarbonization program.

Transition Strategy — Non-Compliant, Fortune 1000 and SBTi

The total addressable market has two ends: non-compliant building owners driven by LL97 penalty avoidance, and Fortune 1000 / SBTi-committed tenants driven by corporate ESG mandates. Together they represent a ~$1.02B annual market.

The Efficient Equation

Aligning LL97 compliance with corporate net-zero goals — every dollar a tenant spends on carbon compliance is one less the building owner needs to spend. Provide an efficient mechanism of value transfer to align with global Scope 3 reporting frameworks and regulated and verified carbon credit assets.

SOLUTION

BENEFIT

NYC Citywide GHG Reduction: 2024–2050

NYC building sector emissions (MtCO₂e) declining from the 2024 baseline of 58 MtCO₂e as each LL97 phase tightens limits. The blue dashed line shows the accelerated impact when Fortune 1000 and SBTi companies proactively cover their carbon footprint.

- LL97 Smoothed

- Smoothed + F1k/SBTi

- LL97 As-Written (Cliff)

Fortune 1000 & SBTi Companies in NYC

Beyond building owners, major corporate tenants face independent ESG obligations — creating a second, voluntary demand stream for compliance assets. These companies occupy space across hundreds of LL97-regulated buildings.

The Fortune 1000 + SBTi segment represents ~24% of total TAM by dollar value, but is disproportionately valuable because these buyers have dual motivation: they are driven by both LL97 compliance obligations AND their own Scope 3 corporate targets — meaning they will pay a premium for verified, DABA-registered assets over generic offsets or NYC-issued credits.

Winning one Fortune 1000 tenant relationship (e.g., JPMorgan, Goldman Sachs, Pfizer, Deloitte, or Accenture) can unlock compliance spend across dozens of buildings in their portfolio simultaneously. SBTi-committed companies are also under intense scrutiny and will specifically seek out institutional-grade assets over credits flagged by the NYC Comptroller as greenwashing risks.

Smoothing the 2030 Cliff

Avoiding market shock through incremental adoption — replacing a single catastrophic liquidity event with a predictable, manageable compliance ramp.

"A smoothed program eliminates the $9.3B single-year liquidity shock, creating a stable environment where institutional-grade carbon assets can thrive."

Cliff vs. Smoothed: 2024–2050

The as-written law creates four separate market shocks — one at the start of each 5-year compliance period. A smoothed approach (5–8% annual tightening) produces a single manageable arc, peaking at ~36% non-compliance around 2037–2038 before declining steadily to net-zero.

- Cliff Scenario

- Smoothed (from 2024)

- Smoothed (from 2027)

Sources: Urban Green Council Benchmarking Update (Dec 2024); NYC Mayor's Office of Climate & Environmental Justice (Sep 2023); GT Law LL97 Analysis (May 2025); NYC DOB. Phase 3–5 limits projected based on LL97's stated 80% reduction by 2050 trajectory. Penalty pool uses $268/tCO₂e × avg 67 tCO₂e excess per non-compliant building.

Four separate market shocks — one every 5 years. Non-compliance jumps from 7% to 57% in a single year at the 2030 threshold. Creates boom-bust cycles that make long-term capital planning impossible.

A single manageable arc — non-compliance rises gradually to a peak of ~36% around 2037–2038, then declines steadily as retrofits accumulate. Both scenarios converge at 5% by 2050.

A 3-year delayed start keeps 2024–2026 flat at ~8%, then ramps smoothly. Peak non-compliance shifts to ~38% around 2040 — slightly higher and later than the 2024 start — but still converges to 5% by 2050. The delay costs ~3 years of early carbon reduction.

Credit Partner Program

To be part of Triangle's credit distribution program, partners must demonstrate a comprehensive commitment to decarbonization — not just building-level compliance — driven by GHG reporting for consistency.

This standard ensures Triangle's distribution network is composed of credible, committed partners — protecting the integrity of the credit market and the value of Triangle-regulated assets.

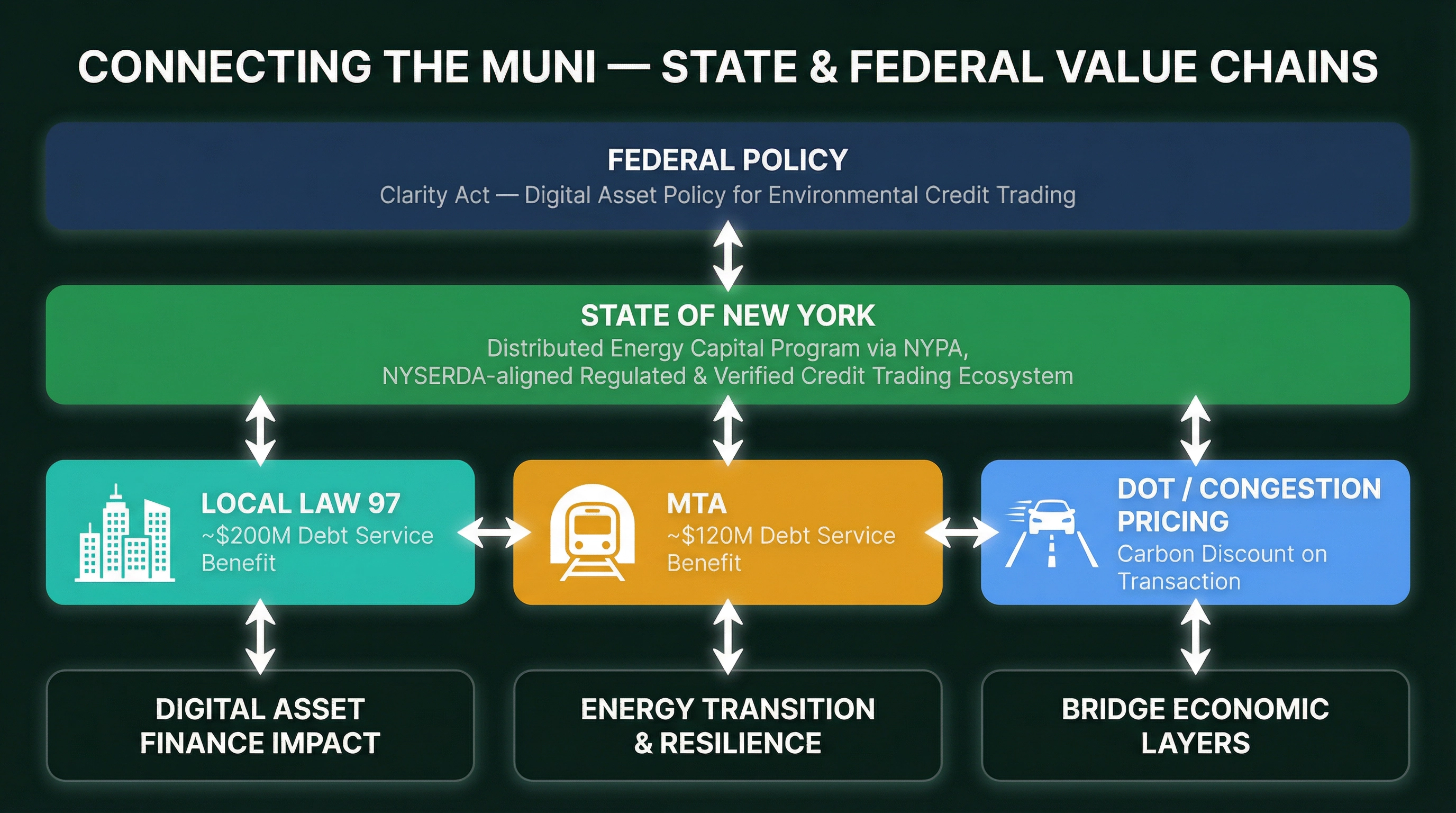

Connecting the Value Chain

Aligning State and Federal value chains to drive shared economic policy — three city programs linked to create a self-reinforcing framework for energy transition, debt cost reduction, and resilience adaptation.

Tri-State Regulated & Verified Environmental Credit Market for LL97 / Scope 3 reporting for F1k & SBTi companies.

Capture ~$200M in annual debt service cost savings through the 15bps greenium on NYC muni bonds unlocked by LL97 compliance and verified carbon credit assets.

Link to the MTA micro-site program — employee commuting and business travel carbon reduction unlocks ~$120M in annual MTA debt service cost savings through green bond pricing.

Fortune 1k / SBTi companies pay for employee commuting carbon associated with congestion pricing transactions — providing a discount mechanism that covers the carbon cost. Cost benefit TBD.

Verified carbon credit assets underpin a new layer of digital finance infrastructure — linking compliance obligations to tradeable, regulated instruments.

Combines City, State, and Federal policy into a unified energy transition framework — NYPA clean electrons, LL97 demand reduction, and MTA electrification working in concert.

Sound federal policy aligned with state power distribution, sharing the economic cost across the drivers of the state economy — building owners, corporate tenants, and transit riders.

Be Part of NYC's

Carbon Transition

Triangle Digital is building the Tri-State Regulated & Verified Environmental Credit Market — connecting building owners, Fortune 1000 tenants, and city government into a single, efficient compliance ecosystem.

Tell us about your organization and we'll schedule a 30-minute overview of the program and your compliance pathway.

Data Sources & Assumptions

92% of buildings compliant with 2024 limits; 43% of all buildings already meet 2030 limits; 57% will not meet 2030 limits without action.

63% of large buildings were already exceeding 2030 targets at time of publication.

2024–2029: ~11% non-compliant; 2030–2034: up to 80% non-compliant if no upgrades made; 2035+: deep retrofits required.

Penalty rate: $268 per metric ton of CO₂e over the applicable emissions limit. Net-zero target: 2050.

10,000 companies globally have now committed to Science Based Targets, with ~300 estimated to have material NYC presence.

NYC-issued credits present significant greenwashing risk; do not factor in electricity reductions in estimates.

Phase 3–5 emissions limits are projected based on LL97's stated 80% reduction by 2050 trajectory, as specific limits have not yet been published by NYC DOB.

Penalty pool calculation uses $268/tCO₂e × average 67 tCO₂e excess per non-compliant building (conservative estimate).

Smoothed scenario models 5–8% annual tightening with no 5-year step changes, analogous to SEC phased disclosure rules.

Fortune 1000 NYC office footprint: 43 F500 HQ × avg 1M sq ft + 150 F500 satellite offices × avg 350K sq ft + 66 F1000 HQ × avg 500K sq ft + 200 F1000 satellite offices × avg 200K sq ft = ~140M sq ft total.

SBTi NYC presence estimated at ~3% of 10,000 global signatories = ~300 companies × 150K sq ft avg = ~45M sq ft. Combined unique Fortune 1000 + SBTi footprint ~165M sq ft (accounting for ~20M sq ft overlap between F1000 and SBTi companies). Voluntary Scope 3 TAM = 165M sq ft × $0.75/sq ft = ~$124M/yr.

F500/SBTi Scope 3 voluntary spend estimated at $0.75/sq ft, consistent with voluntary carbon market pricing at $268/ton.